🌟 What is Share-Based Compensation?

It’s a form of employee reward where a company gives its employees shares of the company’s stock (or options to buy stock) as part of their compensation package. The goal is to align the interests of employees and shareholders. If the company does well and the stock price goes up, the employees benefit too!

🌟 Why Do Companies Offer Share-Based Compensation?

-

Motivation: Employees are encouraged to work harder, knowing their efforts can increase the company’s value and stock price.

-

Retention: Share-based compensation usually has vesting conditions (you only get the shares after working for a certain period). This helps keep employees around longer.

-

Cash Flow: It allows companies to conserve cash by paying part of compensation in stock instead of cash.

🌟 Types of Share-Based Compensation:

✅ Stock Options:

-

Employees get the right to buy company shares at a fixed price (exercise price) in the future.

-

If the stock price goes up, they can buy at the lower exercise price and sell at the higher market price (profit!).

✅ Restricted Stock Units (RSUs):

-

Employees receive actual company shares, but they’re subject to vesting conditions (e.g., working for 3 years).

✅ Employee Stock Purchase Plans (ESPPs):

-

Employees can buy shares at a discounted price through payroll deductions.

🌟 Accounting for Share-Based Compensation:

-

Companies must estimate the fair value of the shares/options at the grant date (when awarded) using valuation models like the Black-Scholes Model for options.

-

This value is then expensed over the vesting period (the period employees must stay to earn the shares).

-

The expense is shown in the income statement, reducing net income, and a corresponding increase in equity is recorded in the balance sheet.

🌟 Key Terms:

| Term | Meaning |

|---|---|

| Grant Date | Date the company awards the stock/options. |

| Vesting Period | Time the employee must wait to earn the shares. |

| Exercise Price | The fixed price at which options can be bought. |

| Fair Value | The estimated value of shares/options at grant. |

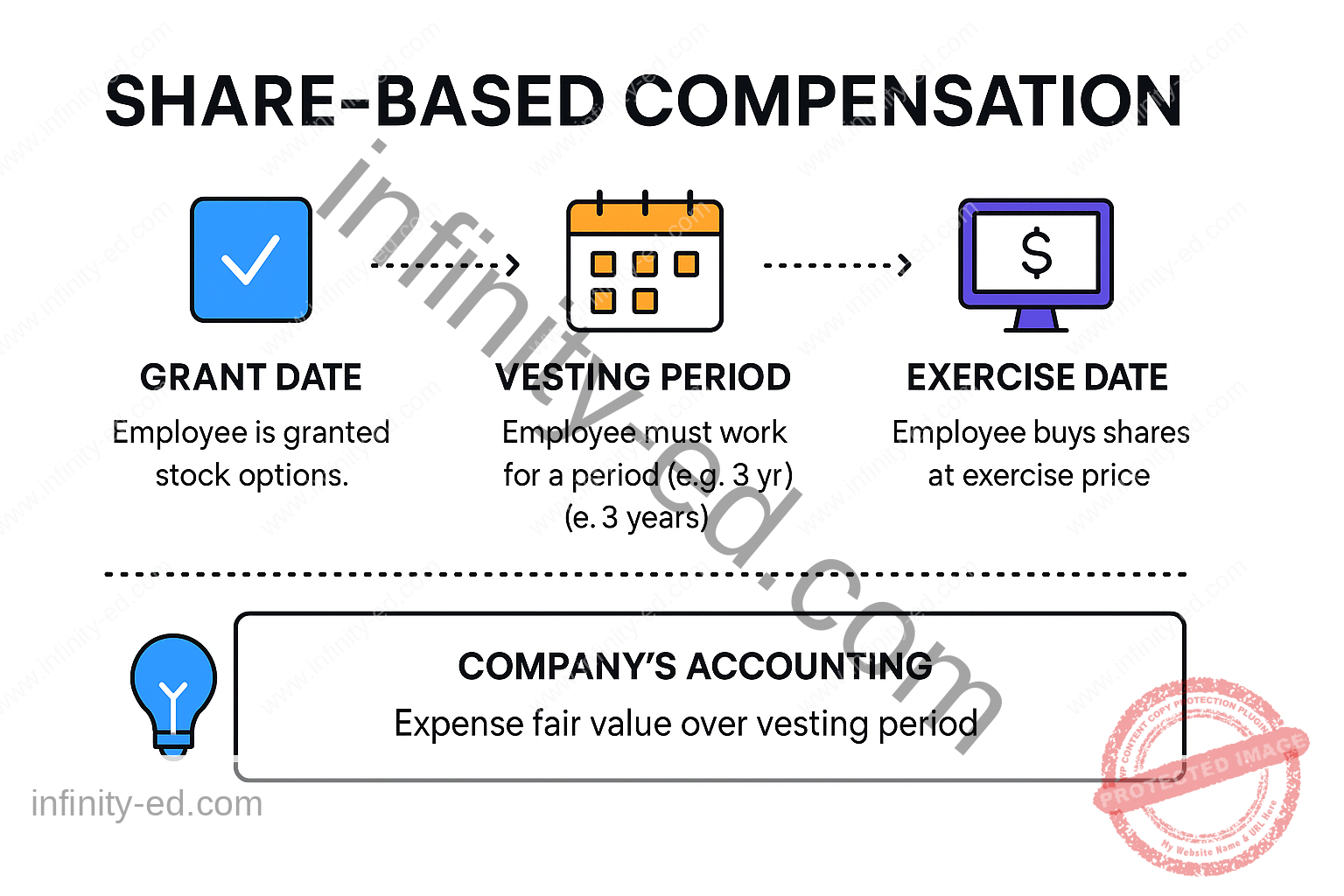

🌟 Diagram: How Share-Based Compensation Works

[Grant Date] ──────────▶ [Vesting Period] ──────────▶ [Exercise Date]

(Stock Awarded) (Employee earns right) (Employee buys shares)Exercise price = $10

Vesting period = 3 years

🌟 Example: Share-Based Compensation in Action

🔹 A company gives an employee 100 stock options at an exercise price of $10 (the price they’ll pay later to buy the shares).

🔹 These options vest over 3 years (meaning they must work 3 years to earn the right to exercise them).

🔹 After 3 years, if the stock price is $25, the employee can:

-

Buy 100 shares at $10 each (total cost = $1,000).

-

Sell 100 shares at $25 each (total proceeds = $2,500).

-

Profit = $2,500 – $1,000 = $1,500.

✅ The company records the fair value of the options as an expense over the 3 years. For example, if the fair value is $5 per option:

-

Total compensation expense = 100 x $5 = $500.

-

The company records $500 ÷ 3 = ~$167 each year for 3 years in its income statement.

🌟 Summary Table

| Step | What Happens |

|---|---|

| Grant Date | Employee is granted stock options. |

| Vesting Period | Employee must work for a period (e.g., 3 years). |

| Exercise Date | Employee buys shares at exercise price (e.g., $10). |

| Share Price Increase | Employee profits if share price > exercise price. |

| Company’s Accounting | Expense fair value over vesting period. |