A Simple Explanation of Pension Accounting

Pension accounting is about how a company reports its pension obligations and assets in its financial statements, based on two major standards:

-

IFRS (International Financial Reporting Standards)

-

US GAAP (United States Generally Accepted Accounting Principles)

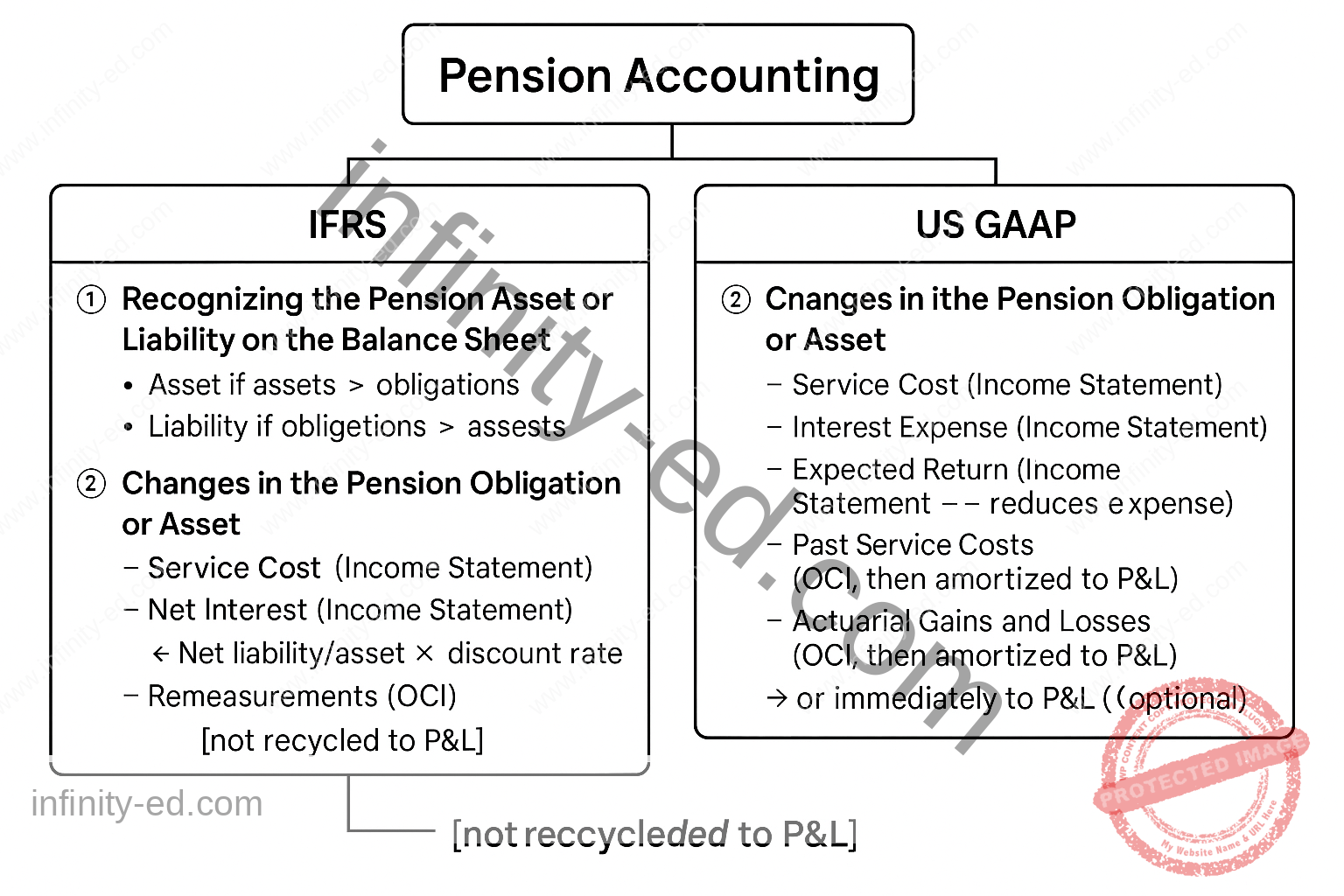

✅ 1️⃣ Recognizing the Pension Asset or Liability on the Balance Sheet

Regardless of IFRS or US GAAP, the company compares:

-

Present Value of Pension Obligation (PBO) → The estimated value of future pension payments (discounted to present).

-

Fair Value of Plan Assets → The current market value of the investments held to fund pensions.

The result:

| Scenario | Accounting Treatment |

|---|---|

| Obligations > Assets (Deficit) | Recognized as a long-term liability (Non-current liability). |

| Assets > Obligations (Surplus) | Recognized as an asset on the balance sheet. |

✅ 2️⃣ How Changes in the Pension Obligation or Asset are Recorded?

Under IFRS:

There are 3 key components:

| Component | What It Means | Where It’s Reported |

|---|---|---|

| 1️⃣ Service Cost | Benefits earned by employees in the current year + past service changes | Income Statement (P&L) |

| 2️⃣ Net Interest | Interest on the net pension liability or asset:Net Pension Liability/Asset × Discount Rate |

Income Statement (P&L) |

| 3️⃣ Remeasurements | Actuarial gains/losses from assumptions or experience, and differences in actual returns | OCI (Other Comprehensive Income), not recycled to P&L later. |

Under US GAAP:

There are 5 components:

| Component | Where It’s Reported |

|---|---|

| 1️⃣ Service Cost | Income Statement (P&L) |

| 2️⃣ Interest Expense | Income Statement (P&L) |

| 3️⃣ Expected Return on Plan Assets | Reduces pension expense in Income Statement (P&L) |

| 4️⃣ Past Service Costs | First in OCI, then amortized over time to P&L |

| 5️⃣ Actuarial Gains and Losses | First in OCI, then amortized over time to P&L (or immediately recognized in P&L if the company chooses). |

✅ Major Differences: IFRS vs. US GAAP

| Item | IFRS | US GAAP |

|---|---|---|

| Net Interest | Single calculation on the net pension amount | Separate: interest on obligations and expected return on assets |

| Remeasurements | OCI only, not recycled to P&L | OCI first, then amortized to P&L (or immediate P&L option) |

| Past Service Cost | Directly to P&L | Initially in OCI, then amortized to P&L |

✅ Quick Example:

A company has:

-

Pension Obligation = $1,000,000

-

Plan Assets = $800,000

Therefore:

-

Net Pension Liability = $200,000 → Reported as a non-current liability.

If the company records actuarial gains of $50,000:

-

Under IFRS → Recorded in OCI only (never goes back to P&L).

-

Under US GAAP → Recorded in OCI, then amortized into P&L over time.